Our ACA Reporting Solution offers three levels of service

Passport Software offers three tiers of service to help simplify Affordable Care Act compliance year-round. We provide much more than just forms and year-end filing.

1- Our ACA Reporting Solution includes IRS-certified Passport™ Affordable Care Act Management Software.

2 – Or, our software users can manage ACA compliance year-round and use our optional IRS-approved proxy submission service.

3 – Lastly, with our Full Service ACA Reporting Solution, we do it ALL for you throughout the year, from employee management to electronic filing.

Our comprehensive ACA Reporting Solution simplifies compliance, tracks coverage and manages employee data throughout the year to help avoid penalties. Passport Software also issues updates as part of its maintenance program to adhere to federal compliance obligations.

Our ACA Reporting Solutions help handle the administrative burden for you. With our ACA Reporting Software solution, you can import employee information, quickly generate every employee ACA record, and you get all the tools to avoid IRS penalties throughout the year.

Optional integrated payroll software is available.

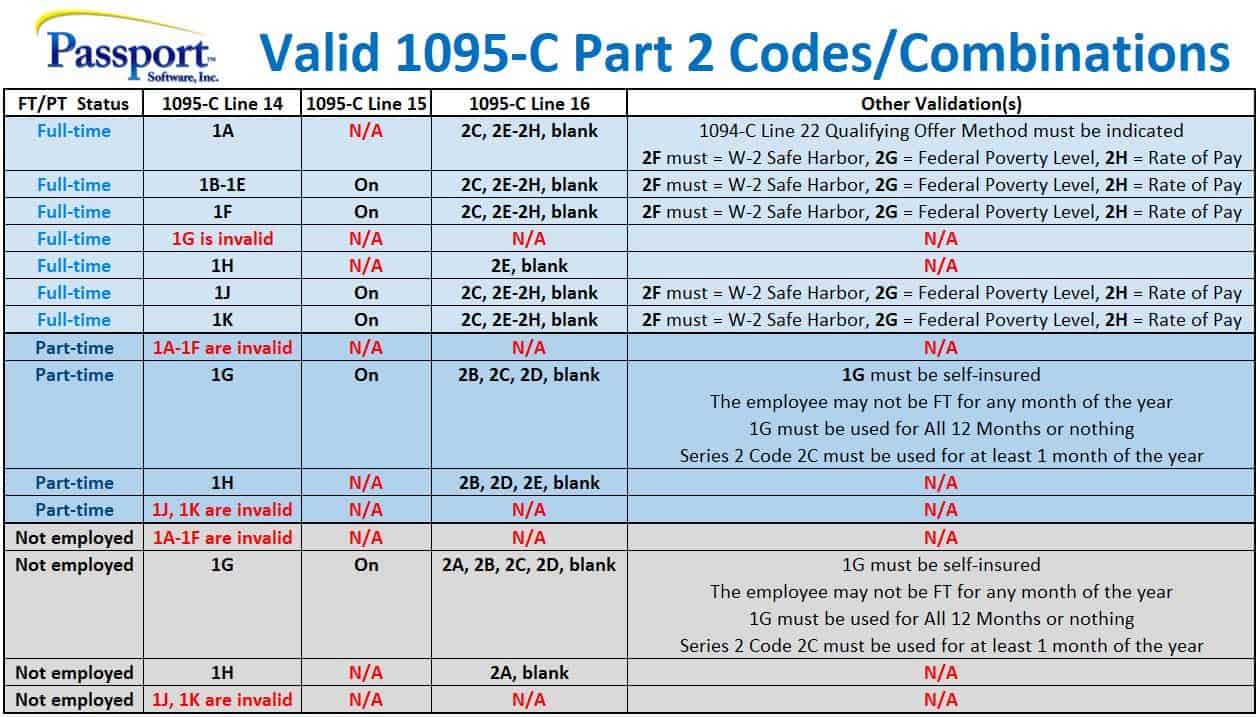

The toughest part about the 1095-C is Part 2 (lines 14-16).

Line 14 instructions are written in typical IRS-speak, but actually not too difficult once you get through everything. Most companies use just 2 codes; 1H, which means coverage was not offered (hopefully with good reason), or 1E, which indicates qualifying and affordable coverage was available to the employee, and that qualifying coverage was also available to the spouse, and all dependents.

The family portion does not need to meet the affordability standards. Because of this, it makes sense to offer it to all family members of a full-time employee. Once you meet that standard, reporting is simplified because even for single employees you may use 1E and never have to make the distinctions between 1B (employee only), 1C (employee and dependents), and 1D (employee and spouse).

Contribution Amount

For the contribution amount on line 15, you need to disassociate your answer on the previous line. People tend to have “employee, spouse, dependents” stuck in their brain because that’s how they just answered the last question, but that’s not what the IRS is looking for here. They want to know “What is the employee share of the least expensive employee-only qualifying plan?”

What could the employee have enrolled in? It is not asking for the actual amount they are paying for a better or family inclusive plan.

Most of the confusion on line 16 stems from employees who waive coverage. The IRS instructions never uses the specific terms “waived” or “declined”, but the normal codes to use here are 2F, 2G, or 2H, depending on which method (safe harbor) is used to estimate an employee’s income. These three codes mean that the coverage offered to the employee was affordable using the safe harbor. (2F = W-2 Wages, 2G = the Federal Poverty Level, and 2H = Rate of Pay.)

Form 1095-C Codes

As mentioned earlier, many companies will only use 1E and 1H for line 14. The full legal wording may be found directly from the IRS, but we have tried to simplify the language a little here:

1A. Qualifying Offer: Offer of affordable Minimal Essential Coverage providing Minimum Value to the full time (FT) employee and at least MEC offered to spouse and dependent(s). Important: Before you use Code 1A, note that it differs from 1B-1E. 1A applies when the ALE member meets the certification guidelines and checks box A on line 22 of the summary transmittal form (1094-C). Also, with the 1A certification, no contribution amount is entered on line 15. You may not use code 1A if the monthly employee contribution amount is greater than $93.18. As this amount may change from year to year, review the IRS documentation for confirmation.

1B. MEC providing minimum value offered to employee only.

1C. MEC providing minimum value offered to employee and at least MEC offered to dependent(s) (not spouse). You may use code 1C even for an employee who does not have dependents.

1D. MEC providing minimum value offered to employee and at least MEC offered to spouse (not dependent(s). You may use code 1D even for an employee who does not have a spouse.

1E. MEC providing minimum value offered to employee and at least MEC offered to dependent(s) and spouse. As noted above, this is the code you would use instead of 1A if you are reporting the cost of monthly coverage on line 15. You may use code 1E even for an employee who does not have a spouse or dependents.

1F. MEC NOT providing minimum value offered to employee or any combination of spouse or dependents.

1G. Offer of coverage to employee who was not a full-time employee for any month of the calendar year and who enrolled in self-insured coverage for one or more months of the calendar year.

1H. No offer or non-qualifying offer of coverage.

1J. Same as 1D except conditionally offered to the spouse.

1K. Same as 1E except conditionally offered to the spouse.

The most common line 16 codes are 2A through 2D, plus the 2F/G/H which matches your safe harbor.

2A. Employee not employed during any day of the month.

2B. Employee not a full-time employee and did not enroll in MEC, if offered for the month. Enter code 2B also if the employee is a full-time employee for the month and whose offer of coverage (or coverage if the employee was enrolled) ended before the last day of the month solely because the employee terminated employment during the month (so that the offer of coverage or coverage would have continued if the employee had not terminated employment during the month). Also use this code for January if the employee was offered health coverage no later than the first day of the first payroll period that begins in January.

2C. Employee enrolled in coverage offered. Enter code 2C for any month in which the employee enrolled in health coverage offered by the employer for each day of the month, regardless of whether any other code in Code Series 2 might also apply (for example, the code for a section 4980H affordability safe harbor).

2D. Employee in a section 4980H(b) Limited Non-Assessment Period. If an employee is in an Initial Measurement Period (IMP), enter code 2D, and not code 2B. For an employee in a section 4980H(b) Limited Non-Assessment Period for whom the employer is also eligible for the multi-employer interim rule relief for the month code 2E, enter code 2E and not code 2D.

2E. Multi-employer interim rule relief. Enter code 2E for any month for which the multi-employer interim guidance applies for that employee.

2F. Enter code 2F if the employer used the section 4980H Form W-2 (wage) safe harbor to determine affordability.

2G. Enter code 2G if the employer used the section 4980H federal poverty line safe harbor to determine affordability.

2H. Enter code 2H if the employer used the section 4980H rate of pay safe harbor to determine affordability.

2I. is no longer valid.

A blank Series 2 Code is a valid option in rare cases where nothing else applies.

Click Image to View

Myths about the 1095-C

The thought (or hope) that ACA reporting is going away. Even under the recent attempts to “repeal and replace” there was no indication that company reporting would disappear in the near future. For right now, this is the law of the land and there are serious penalties for late filing or “intentional disregard”.

Most confusing thing about the 1095-C?

Aside from the Part 2 information which we already discussed, electronic filing (which is required for any company with 250 or more 1095-C forms) is virtually impossible without a professional service or 1095-C software. Even the application for a Transmitter Control Code which is your permission to file electronically is typically a minimum 3-week, multi-stage process.

A Common Question

The big one from an employee is “When was I offered coverage?” Companies should keep good records. Other than that, I recommend distributing the employee copies (or better yet, draft versions) as early as possible. If you discover any mistakes in the data, even a name-change or incorrect Social Security Number, it is much easier to correct it before you file the official copies with the IRS.