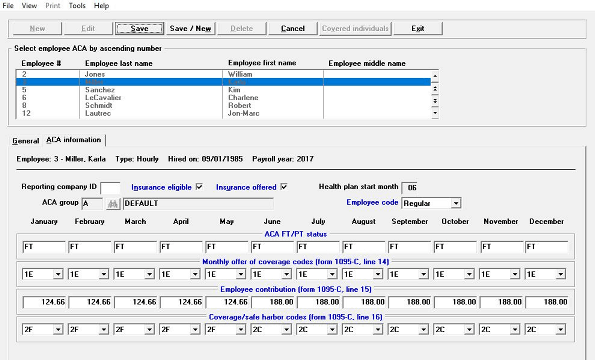

ACA Software and Services: Compliance for Your Growing Company

ACA Support for Companies Growing into ALE Status

Hello again,

This post is for companies that may be growing to become Applicable Large Employers (ALEs) required to comply with the Affordable Care Act. We hope you find it useful.

Could your company grow and become an Applicable Large Employer (ALE) in 2021?

If your company is positioning itself to grow in 2021 and beyond, exciting opportunities and challenges await. It’s difficult to plan for every contingency that will come with growth.

However, setbacks such as accidental violations of the ACA guidelines can be minimized or avoided altogether with just a little preparation. Here is an overview that may help.

ALEs

If your company’s growth plan includes increasing the number of staff, you will want to monitor to see if your company becomes an “applicable large employer”, often referred to as an “ALE.”

An ALE is defined as a company with 50 or more full-time employees working at least 30 hours per week (or equivalents when adding together part-time hours).

If your company were to expand and employ 50 or more full-time workers or equivalents, your company should be prepared to offer coverage to at least 95 percent of the full-time employees.

Businesses with fewer than 50 workers are exempt from the employer mandate, but if they chose to offer health coverage it must meet certain ACA specifications.

ACA Affordability Requirement

The ACA’s affordability requirement is defined as the highest percentage of household income an employee can be required to pay for monthly health insurance plan premiums, based on the least expensive employer-sponsored plan offered that meets the ACA’s minimum essential coverage requirements.

The affordability percentage is adjusted annually for inflation. For 2021 it rose to 9.83 percent of an employees’ household income.

Because your company won’t know your employees’ household incomes, there are three affordability safe harbors you, as an applicable large employer (ALEs) can use to determine if the annual affordability threshold is being met, using (i) W-2 wages, (ii) rate of pay, or (iii) federal poverty level.

Penalties

Here is an outline of the penalties associated with non-complying with the ACA guidelines. ACA guidelines include what are commonly called “Play or Pay” penalties. These currently include:

The Section 4980H(a) Penalty – The (a) penalty applies when the ALE does not offer minimum essential coverage to at least 95 percent of its full-time employees in any given calendar month and at least one full-time employee receives a premium tax credit to help pay for coverage through an ACA marketplace exchange. (Remember: Full-time employees are those who average 30 or more hours of work per week. The penalty is waived for the first 30 full-time employees.)

Employees with household income between 100 percent and 400 percent of the federal poverty level are eligible for tax credits for exchange coverage if they do not have access to affordable employer-sponsored coverage that provides at least minimum value (meaning the plan pays at least 60 percent of the cost of covered benefits).

– The (a) penalty in 2020 is $214.17 per month ($2,570 annualized), multiplied by all full-time employees (minus the first 30). For 2021, the penalty increases to $225 per month ($2,700 annualized).

The Section 4980H(b) penalty – The (b) penalty applies when the ALE does offer coverage to at least 95 percent of full-time employees, but each full-time employee was not offered an option of “minimum essential coverage” that was “affordable” and provided “minimum value.” The penalty is triggered when a full-time employee of an ALE declines an offer of noncompliant coverage and instead enrolls in subsidized coverage on the ACA marketplace exchange.

– The B penalty for 2020 is $321.67 per month ($3,860 annualized) per full-time employee receiving subsidized coverage on the ACA marketplace exchange. For 2021, the penalty increases to $338.33 per month ($4,060 annualized).

The IRS sends Letter 226J to inform ALEs of their potential liability for an employer shared-responsibility payment.

Failure to Pay

What happens when a company does not pay ACA penalties assessed by the IRS? The IRS possesses enforcement powers under the ACA, to levy and to lien.

According to the IRS, the definitions of levy and lien are as follows:

“A levy is a legal seizure of your property to satisfy a tax debt. Levies are different from liens. A lien is a legal claim against your property to secure payment of your tax debt, while a levy actually takes the property to satisfy the tax debt.”

“A federal tax lien comes into being when the IRS assesses a tax against you and sends you a bill that you neglect or refuse to pay.”

According to the ACA Times, “The IRS utilizes the term ‘seizure’ interchangeably with levy. Practically, there is no difference as far as the agency is concerned. The bottom line is that the IRS may seize your organization’s property and force a sale to pay for your ACA liability. Funds within corporate bank accounts may also be levied and applied to the liability. A federal tax lien can likewise have devastating effects on business operations. Among other things, a lien gives public notice to creditors concerning the ACA liability. The lien may also be reported to credit reporting agencies, creating obstacles to accessing credit, securing capital, and impact commercial tenant/landlord relations.”

Expert guidance ahead of time can avoid the need for penalty consultation when it’s too late.

With planning, ACA guideline compliance can be less of a headache. Passport Software offers a free consultation service. If you are planning for expansion in 2021, we invite you to call us.

Call 800-969-7900 for ACA questions in general, or to learn more about our ACA Software, ACA Full Service option, or our penalty relief consultation services. Or, contact us – we are here to help